Mortgage Investment Corporation Things To Know Before You Get This

Table of ContentsHow Mortgage Investment Corporation can Save You Time, Stress, and Money.Some Known Details About Mortgage Investment Corporation Not known Details About Mortgage Investment Corporation More About Mortgage Investment CorporationRumored Buzz on Mortgage Investment Corporation

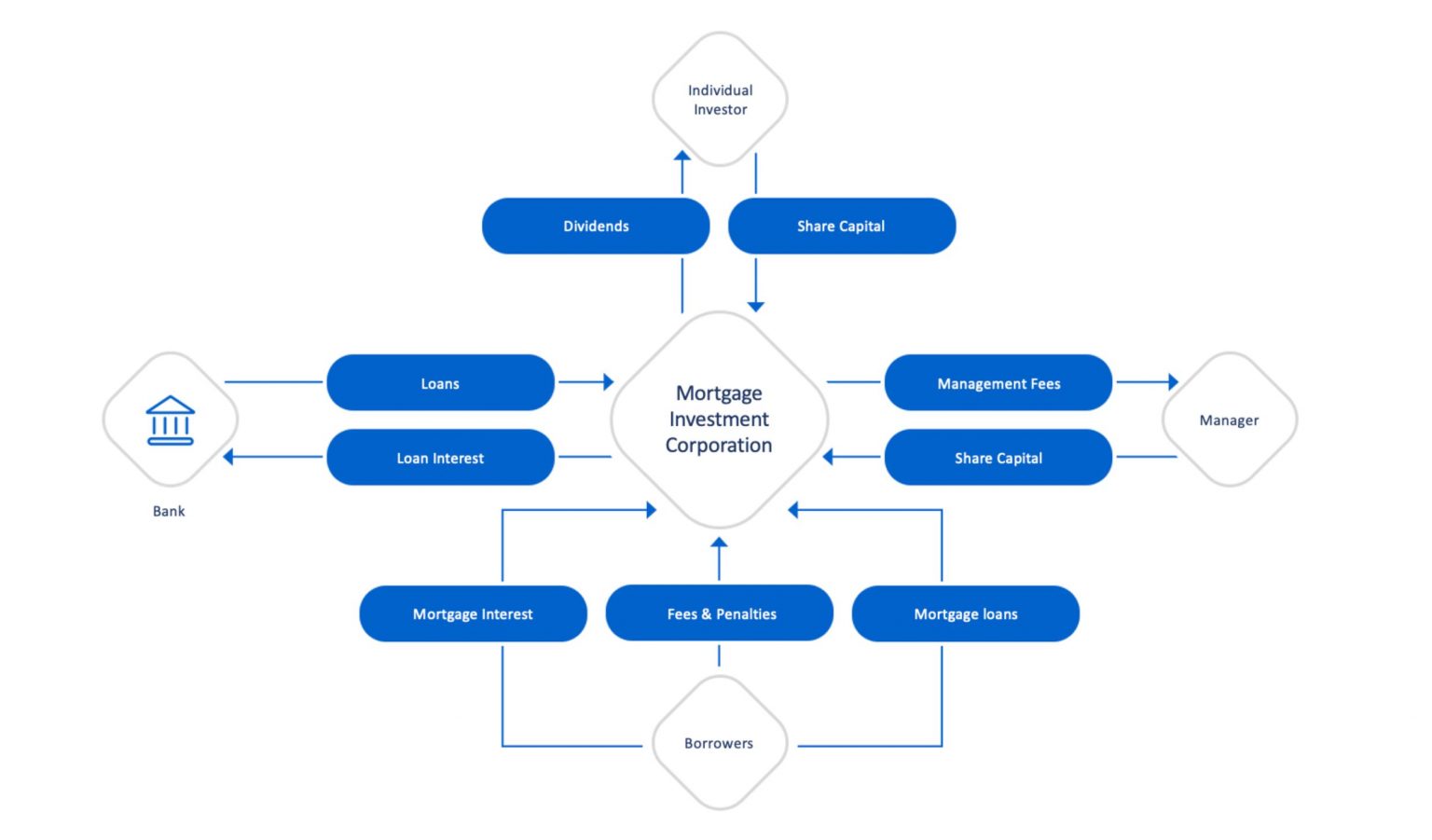

Does the MICs credit committee testimonial each home mortgage? In most situations, mortgage brokers take care of MICs. The broker needs to not function as a participant of the credit report board, as this puts him/her in a direct conflict of passion considered that brokers normally earn a commission for positioning the home loans. 3. Do the directors, members of credit rating committee and fund supervisor have their own funds spent? Although an of course to this concern does not offer a safe financial investment, it ought to provide some raised safety if analyzed along with various other sensible lending plans.Is the MIC levered? Some MICs are levered by an economic institution like a legal financial institution. The banks will certainly accept certain home loans possessed by the MIC as security for a credit line. The M.I.C. will then borrow from their line of credit and provide the funds at a greater price.

This must offer further scrutiny of each mortgage. 5. Can I have copies of audited monetary declarations? It is vital that an accounting professional conversant with MICs prepare these declarations. Audit procedures must ensure strict adherence to the policies mentioned in the details bundle. Thanks Mr. Shewan & Mr.

Little Known Questions About Mortgage Investment Corporation.

Last upgraded: Nov. 14, 2018 Couple of financial investments are as helpful as a Home loan Investment Company (MIC), when it comes to returns and tax obligation benefits. Since of their corporate structure, MICs do not pay revenue tax obligation and are lawfully mandated to disperse all of their earnings to financiers. MIC returns payouts are dealt with as passion earnings for tax obligation purposes.

This does not imply there are not risks, yet, typically talking, whatever the more comprehensive stock exchange is doing, the Canadian property market, especially major cities like Toronto, Vancouver, and Montreal does well. A MIC is a company formed under the policies set out in the Revenue Tax Obligation Act, Area 130.1.

The MIC earns earnings from those mortgages on interest fees and general charges. The real charm of a Mortgage Investment Corporation is the yield it offers financiers contrasted to other set earnings financial investments. You will have no problem discovering a GIC that pays 2% for an one-year term, as government bonds are similarly as low.

The smart Trick of Mortgage Investment Corporation That Nobody is Talking About

A MIC needs to be a Canadian company and it should invest its funds in mortgages. That stated, there are times when the MIC finishes up possessing the mortgaged building due to foreclosure, sale arrangement, and so on.

A MIC will certainly gain interest revenue from home mortgages and any type of money the MIC has click for info in the bank. As long as 100% of the profits/dividends are provided to shareholders, the MIC does not pay any earnings tax. As opposed to the MIC paying tax obligation on the rate of interest it gains, shareholders are accountable for any tax.

The Of Mortgage Investment Corporation

And Deferred Plans do not pay any tax on the rate of interest they are approximated to obtain - Mortgage Investment Corporation. That claimed, those who hold TFSAs and annuitants of RRSPs or RRIFs might be hit with specific penalty taxes if the investment in the MIC is thought about to be a "prohibited financial investment" according to Canada's tax code

They will certainly ensure you have found a Home loan Investment Company visite site with "qualified financial investment" standing. If the MIC certifies, maybe really valuable come tax time considering that the MIC does not pay tax on the rate of interest earnings and neither does the Deferred Strategy. Extra generally, if the MIC fails to fulfill the demands established out by the Revenue Tax Act, the MICs income will certainly be strained prior to it gets dispersed to shareholders, lowering returns substantially.

It shows up both the genuine estate and securities market in Canada are at perpetuity highs On the other hand yields on bonds and GICs are still near record lows. Also cash is losing its charm because energy and food rates have pushed the rising cost of living rate to a multi-year high. Which begs the concern: Where can we still find value? Well I believe I have the solution! In May I blogged about looking right into home mortgage investment corporations.

The 10-Minute Rule for Mortgage Investment Corporation

Several effort Canadians that desire to acquire a residence can not obtain home mortgages from typical financial institutions due to the fact that probably they're self used, or do not have an established credit rating yet. Or possibly they want a short-term car loan to develop a huge property or make some improvements. Financial institutions have a tendency to ignore these possible debtors because self used Canadians do not have stable revenues.